Over half of non-retired Americans have a defined contribution pension plan through their employer (source: Federal Reserve), with the most common types being 401(k) and 403(b) plans.

These employer-sponsored plans can be an excellent vehicle for individuals to save on taxes and put money aside to create a secure retirement.

Unfortunately, many people in the U.S. do not have a clear understanding of this type of investment account. According to a recent survey by Beyond Finance, 43% of Americans do not know what a 401(k) is.

If that many people are unfamiliar with one of the most popular retirement plans, it is likely that an even greater knowledge gap exists when it comes to understanding the underlying investment options within the plans.

Popularity of target date funds

Retirement plans can vary greatly in their investment offering, but often included are a selection of target date funds. Not only are they commonly offered, but they are also popular among participants. According to the Investment Company Institute’s 2023 fact book (Figure 8.8), 59% of 401(k) participants have invested in target date funds at some point.

Choosing investments can be a difficult and stressful process, so it is no surprise that this type of product is popular, given it offers investors a single-fund solution (as opposed to having to select a bunch of different funds).

How a target date fund works

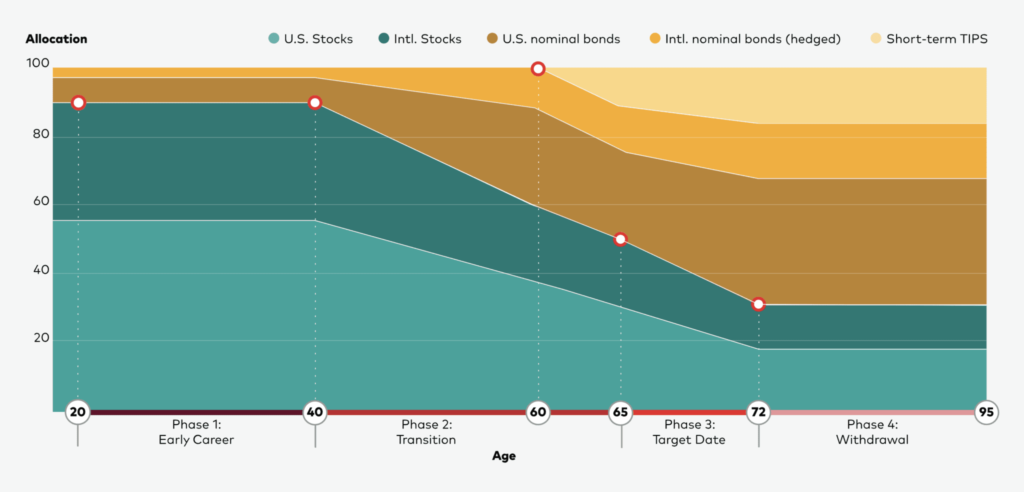

A target date fund combines several types of assets such as stocks, bonds, and cash, into a single investment fund and adjusts its mix over time based on a designated target date. In most cases the investor will pick a target date (a given year) that is close to when they plan to retire. These funds start off more aggressive with a higher concentration in stocks (and less in bonds) and they gradually become more conservative as the retirement year approaches. This shift in allocation over time is referred to as a glide path.

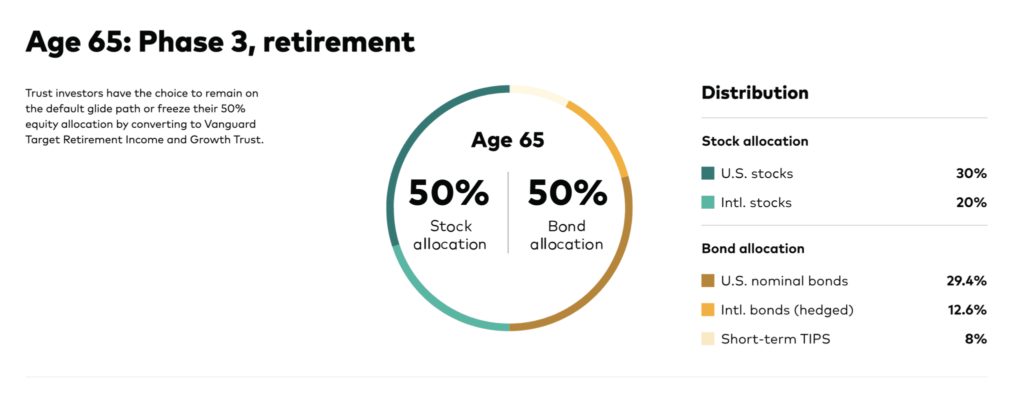

To help illustrate, below is an example that shows Vanguard’s target date fund glide path.

Benefits of target date funds

Simple, diversified, risk management

Perhaps the greatest benefit is that target date funds offer simplicity. In one convenient investment solution, an investor can achieve diversification and investment-risk management as they progress toward retirement.

The funds achieve diversification by investing in multiple types of assets within the broader stock and bond categories (e.g., U.S. and international stocks of varying sizes, corporate bonds, Treasury bonds, etc.). They are professionally managed and mitigate risk by rebalancing and reducing exposure to stocks over time [note: this will also be discussed as a danger below].

Dangers of target date funds

Too conservative for some (longevity risk)

A primary risk-management feature of a target date fund is its reduction of stock exposure over time. However, depending on the investor, this can lead to a fund being too conservative which may expose investors to longevity risk (the risk of outliving one’s assets). Historically, one of the best ways to beat inflation over the long-term has been to buy and hold stocks. That is why stocks remain a key component of any portfolio that is aiming for long-term growth.

A target date fund is built as a one-size-fits-all solution and arguably errs on the side of being more conservative with the overall blend of stocks and bonds. For some individuals, it may simply be too cautious.

Example: Young investors

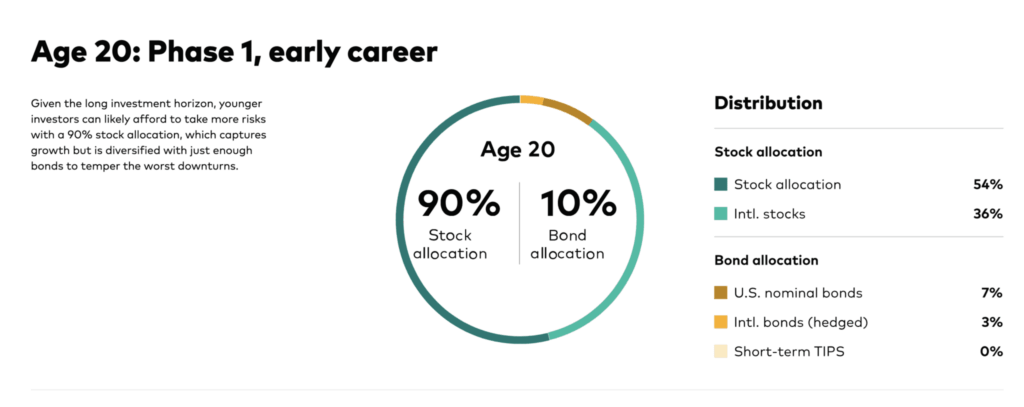

Many young investors will want 100% equity exposure until at least age 40 but most target date funds will start off no more aggressive than 90% equity and 10% bonds. Over several decades, that bond allocation will likely underperform the equity by a substantial margin. For most 25-year-old professionals, the added volatility will not make a difference unless they plan to use the funds before retirement.

Example: Investors approaching retirement

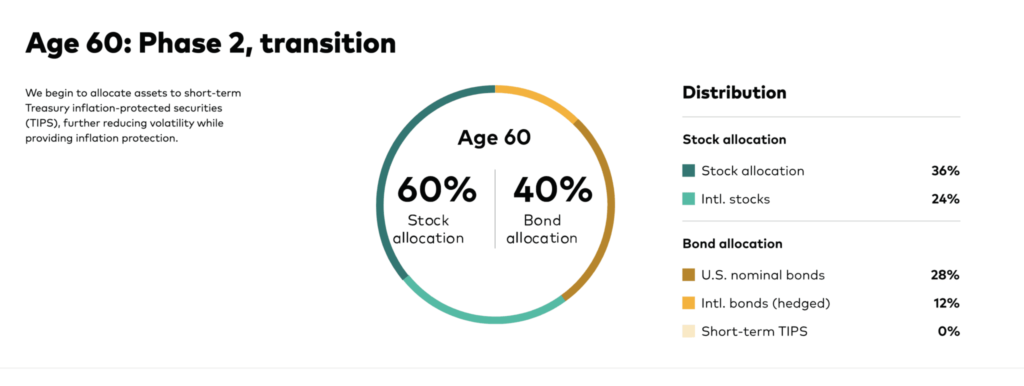

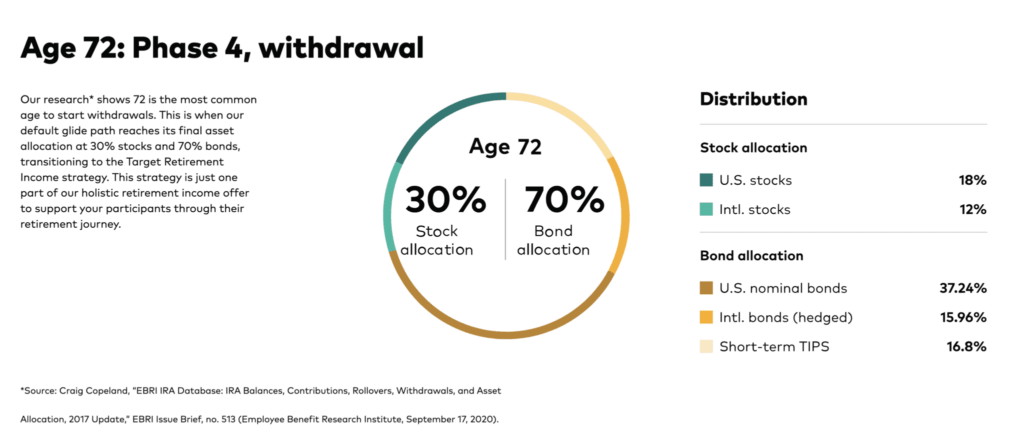

The Vanguard glide path illustrated earlier shows a transition to about 50% stocks and 50% bonds at age 65. [This is not to single out Vanguard – most target date funds will look like this. Vanguard just has it presented very nicely on their website.] That will be fine for some people but too conservative for others. Someone who is retiring at 65 with Social Security and a defined benefit pension may have sufficient retirement income to cover their expenses without taking portfolio withdrawals. That means the 401(k) could be earmarked for a low withdrawal rate farther in the future (e.g., Required Minimum Distributions only), and a blend of 70% stocks and 30% bonds may be more appropriate if that investor has a higher tolerance for risk. Or perhaps this person has a significant allocation to cash and bonds in other investment accounts and needs more in stocks to help keep pace with inflation. It is also possible that the 401(k) is eventually intended to go to heirs or a younger spouse. All of these factors should be considered when selecting one’s investments.

Not all created equally

It is easy to lump target date funds together as one; however, each fund has its own design and characteristics to keep in mind. At a high level, there are funds offered by different investment management companies (e.g., Vanguard, American Funds, Fidelity, Schwab, etc.). There will, of course, be different target dates that correspond to different risk levels. Some funds are actively managed, and some are passive or index funds. Management fees will vary. One should examine these characteristics carefully before selecting a fund.

Investment risks

Of course, target date funds also have inherent investment risk,s but this is a characteristic shared with other types of similar investments.

Other investment options

Pick a target date fund with a later date

One way to temporarily work around the drift of the target date fund is to pick a fund with a date that is further out than your actual retirement. For example, someone retiring in 2035 could pick the 2045 target date fund. This can delay the shift to a more conservative investment allocation. This strategy only makes sense for someone who wishes to take on more investment risk for longer than what their normal target date fund would offer.

Target Risk or Asset Allocation Fund

If you are looking for the simplicity of a target date fund but without the drift to a conservative allocation, see if your plan offers a target risk fund (also known as an asset allocation fund). These are similar to target date funds in that they are a single solution with diversified holdings but they seek to maintain a given level of risk indefinitely (rather than decreasing the stock-to-bond ratio over time).

Professional Management – Plan Advisor

Most company retirement plans will have a professional manager available to some extent. Find out what guidance is available and included in the fees you are already paying.

Professional Management – Outside Advisor

Some plans allow for an outside investment manager to be linked to your account and control the investments. This can be a good fit if you have an existing advisor relationship; just make sure you understand the relationship and fees involved.

Custom/DIY

Assuming your retirement plan has a sufficient selection available, you can always hand-curate an investment portfolio that fits your needs and risk tolerance. This is a good fit for someone who has a good deal of investment knowledge and is willing to research and compare the available funds. It is important to check the fund fees, management style (active vs. passive), and avoid making decisions solely based on past performance.

Conclusion

Target date funds provide a simple and convenient way to achieve diversification and risk management in a single fund. A target date fund is built as a one-size-fits-all product and, just like a one-size-fits-all poncho, it may be a perfect fit, good enough, or totally wrong. It also could fit you now, but not so much several years down the line.

There is nothing inherently wrong with target date funds as a group and in fact they can be the best option for many people. They can be a great fit for someone who does not have the background or resources (or interest!) to investigate and understand their other options. Saving in a target date fund is better than giving into decision paralysis and not saving at all.

The shift to a more conservative allocation over time is a design feature that can also be a hidden danger for investors who are not aware of the asset drift. This can lead to unexpected, disappointing returns and, in the most extreme cases, exposure to longevity risk.

The point of this article is not to dissuade anyone from using a target date fund, but rather to inform of the factors to consider when picking investments and planning for retirement. It is important to review your investments periodically (at least once per year) to make sure they are still aligned with your objectives and risk tolerance. If using a target date fund, look at the materials or website for the fund and be aware of the glide path. Make note of if and when it will become unaligned with your goals and prepare to make changes at that time!