As companies look to cut costs amid the coronavirus pandemic, many of them have or will soon stop matching their employees’ 401(k) contributions.

That can make it harder for you to stay on track with your savings.

During the financial crisis of 2008-09, nearly 1 in 5 employers that offered a 401(k) plan match pulled back their contributions. Some experts expect the current recession to be even more brutal, and many companies have already turned off the spigot into their workers’ nest eggs.

Someone in your human resources department may be able to discuss if your company match is on the chopping block. There might be other ways to find out, as well.

“This is the kind of information that would be released in an earnings conference call to analysts if your employer is publicly traded,” said Scott Puritz, co-founder and managing director of Rebalance, which helps clients with 401(k) rollovers.

Sometimes smoke doesn’t lead to fire. “Many companies during the 2008 crisis warned that they would suspend or end matching and then did not do so,” Puritz said.

“Nevertheless, what’s coming next in terms of the pandemic’s ultimate economic impact is impossible to predict.”

Here are two steps that can help you prepare.

Save more now

If you’re not currently saving enough to get the entire company match, you may want to start doing so, said Arielle O’Shea, investing and retirement specialist at NerdWallet.

“Take advantage of that match while you have it,” O’Shea said.

If you’re already meeting the match, there’s not much you can do because most employers distribute their matches by pay period, said Jean Young, senior research analyst at Vanguard Investment Strategy Group. In other words, you can only get, say, 6% of one paycheck matched at a time.

Yet some employers conduct annual matches, meaning that upping your contributions might generate you a higher company contribution in the end. You’ll want to learn the rules first.

“Talk to your human resources department before you front-load your 401(k),” Puritz said.

Either way, you should consider upping your own contributions if you can while we’re in a downturn. That way, Young said, “You’re able to ‘buy on sale,’ and take advantage of a market recovery.”

Review your plan

If your employer stops contributing to your 401(k) plan, you might want to start saving in an individual retirement account instead, experts say.

“One factor is the quality of the plan,” said Barbara Roper, the director of investor protection at the Consumer Federation of America.

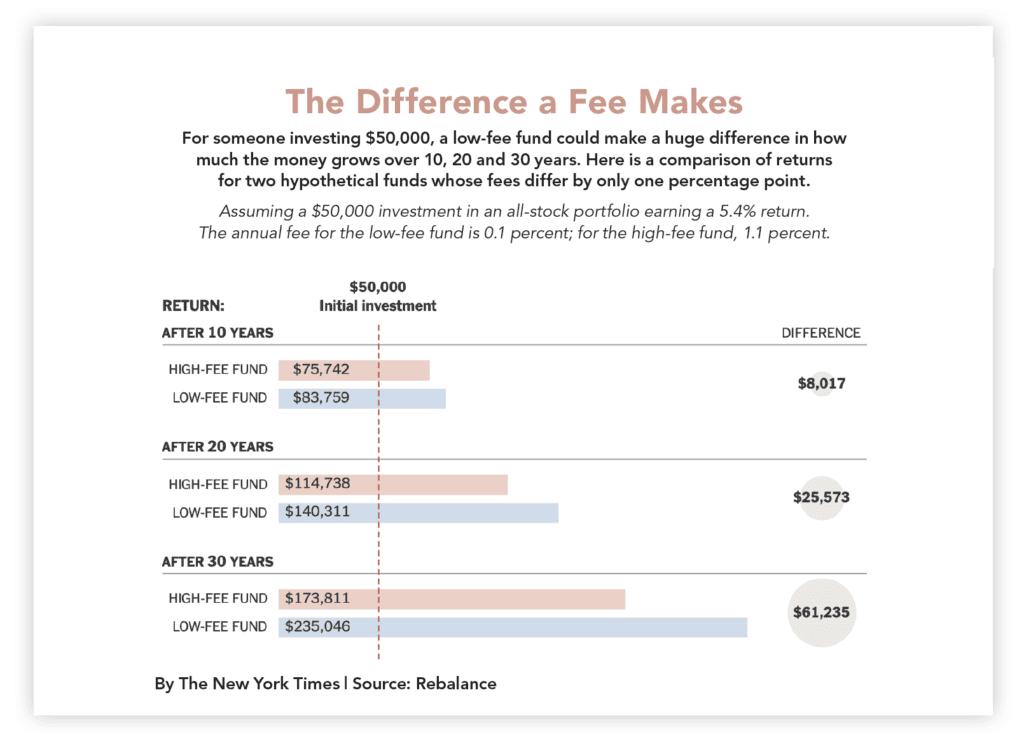

For example, many smaller 401(k) plans are “loaded up with inferior, high-cost options,” Roper said. What you want: a retirement account with low fees.

Wondering what counts as a low fee? Plans typically charge anywhere between 0.1% to 3% of your assets each year. Ideally, you want to be paying somewhere closer to 0.1%.

If not, Roper said, “You may be better off saving for retirement in an individual retirement account.”

Still, the government caps how much you can save in an IRA, and so if you can afford to put away more money, “you’ll want to do that in a 401(k) because the tax advantages are still powerful and the contribution limit is higher,” O’Shea said.

“A thoughtful look at the strategies of eight CEOs who created significant shareholder value. Thorndike distills the characteristics of these CEOs into the ‘outsider’s checklist,’ which can help businesses and investors adopt the right approach to take their game to the next level.”

“A thoughtful look at the strategies of eight CEOs who created significant shareholder value. Thorndike distills the characteristics of these CEOs into the ‘outsider’s checklist,’ which can help businesses and investors adopt the right approach to take their game to the next level.”

“Today’s markets are dominated by a handful of widely held narratives, not underlying fundamentals, with extraordinary monetary policies and curiously timed fiscal stimulus, making it difficult for investors to determine where we are in the long-running economic expansion. This book stresses the importance of using a multidisciplinary framework to solve today’s investment challenges, combining elements of investment philosophy, human decision-making and science (such as physics), along with psychology and complexity theory.”

“Today’s markets are dominated by a handful of widely held narratives, not underlying fundamentals, with extraordinary monetary policies and curiously timed fiscal stimulus, making it difficult for investors to determine where we are in the long-running economic expansion. This book stresses the importance of using a multidisciplinary framework to solve today’s investment challenges, combining elements of investment philosophy, human decision-making and science (such as physics), along with psychology and complexity theory.”

“This begins with the history of the corporation and brings in business, law, economics, science, philosophy and history to suggest how the modern corporation can realize its full potential to help wider society, as well as shareholders.”

“This begins with the history of the corporation and brings in business, law, economics, science, philosophy and history to suggest how the modern corporation can realize its full potential to help wider society, as well as shareholders.”